Promotion

Use code MOM24 for 20% off site wide + free shipping over $45

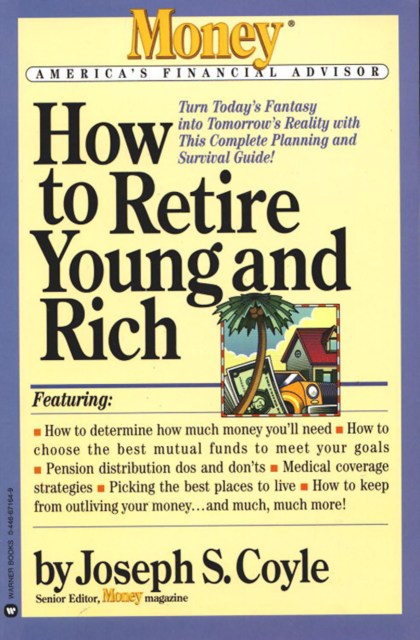

How to Retire Young and Rich

Contributors

By Joseph S. Coyle

Formats and Prices

Price

$8.99Price

$11.99 CADFormat

Format:

ebook (Digital original) $8.99 $11.99 CADThis item is a preorder. Your payment method will be charged immediately, and the product is expected to ship on or around November 15, 2008. This date is subject to change due to shipping delays beyond our control.

Also available from:

Genre:

- On Sale

- Nov 15, 2008

- Page Count

- 208 pages

- Publisher

- Grand Central Publishing

- ISBN-13

- 9780446549691

You May Also Like

Newsletter Signup

By clicking ‘Sign Up,’ I acknowledge that I have read and agree to Hachette Book Group’s Privacy Policy and Terms of Use